Velas más grandes

El script "Velas más grandes" está diseñado para identificar velas con el volumen máximo y la mayor longitud de cuerpo en los gráficos de instrumentos financieros seleccionados durante un período dado. Esta herramienta permite a operadores y analistas identificar eventos de mercado significativos y la reacción de los participantes del mercado.

Funciones clave

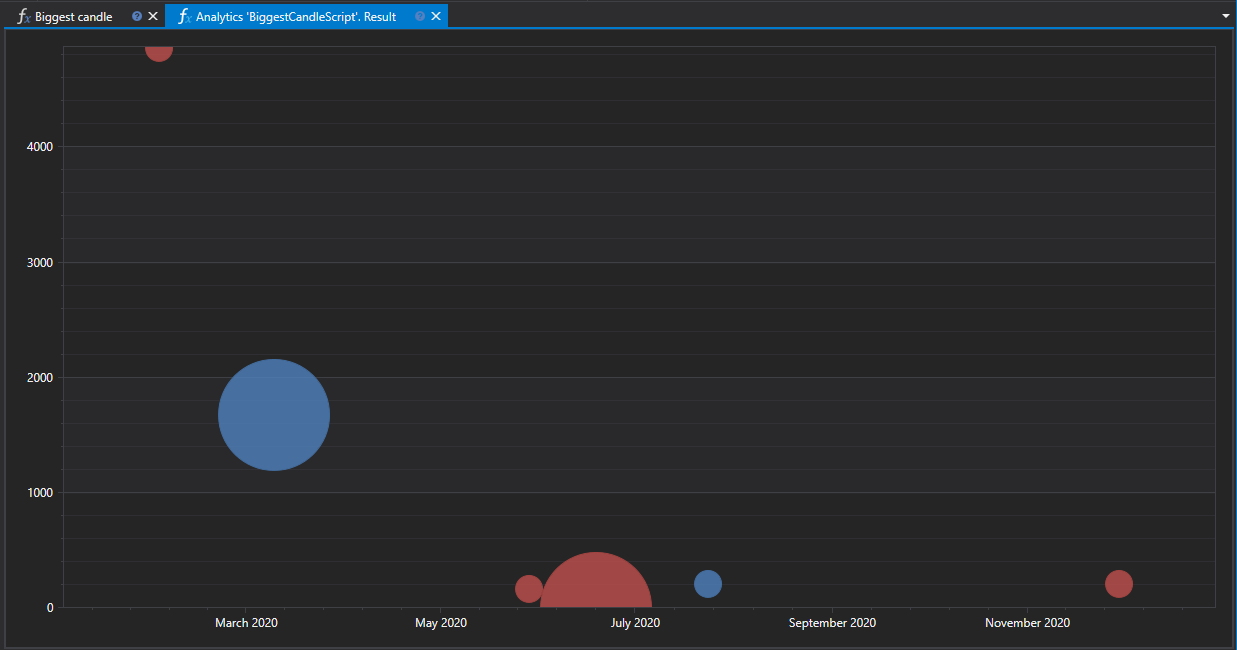

El script analiza un conjunto de instrumentos especificados, busca entre ellos velas con el mayor volumen y longitud de cuerpo, y muestra estos datos en dos gráficos:

- Gráfico de longitud del cuerpo de la vela: muestra velas con la mayor diferencia entre precio de apertura y cierre.

- Gráfico de volumen de negociación: muestra velas con el volumen máximo de negociación durante la existencia de la vela.

Flujo de trabajo

- Selección de instrumentos y período de análisis: determina la lista de instrumentos y el intervalo temporal para análisis.

- Análisis de datos: incluye cargar y analizar datos históricos de velas para identificar las velas con los mayores indicadores.

- Visualización de resultados: las velas encontradas se muestran en gráficos en la interfaz del panel de analítica.

Aplicación

- Análisis de actividad del mercado: ayuda a determinar momentos de mayor actividad de operadores y posibles reversos del mercado.

- Identificación de niveles clave: las velas con volumen y longitud de cuerpo significativos a menudo se forman alrededor de niveles clave de soporte y resistencia.

- Planificación estratégica: la información sobre las velas más grandes puede usarse para planificar puntos de entrada y salida del mercado, considerando la posible volatilidad.

Código del script en C#

namespace StockSharp.Algo.Analytics

{

/// <summary>

/// Script analítico que muestra la mayor vela (por volumen y longitud) para los instrumentos especificados.

/// </summary>

public class BiggestCandleScript : IAnalyticsScript

{

Task IAnalyticsScript.Run(ILogReceiver logs, IAnalyticsPanel panel, SecurityId[] securities, DateTime from, DateTime to, IStorageRegistry storage, IMarketDataDrive drive, StorageFormats format, DataType dataType, CancellationToken cancellationToken)

{

if (securities.Length == 0)

{

logs.LogWarning("No hay instrumentos.");

return Task.CompletedTask;

}

var priceChart = panel.CreateChart<DateTimeOffset, decimal, decimal>();

var volChart = panel.CreateChart<DateTimeOffset, decimal, decimal>();

var bigPriceCandles = new List<CandleMessage>();

var bigVolCandles = new List<CandleMessage>();

foreach (var security in securities)

{

// detener el cálculo si el usuario cancela la ejecución del script

if (cancellationToken.IsCancellationRequested)

break;

// obtener almacenamiento de velas

var candleStorage = storage.GetCandleMessageStorage(security, dataType, drive, format);

var allCandles = candleStorage.Load(from, to).ToArray();

// la primera ordenada por volumen descendente será nuestra vela más grande

var bigPriceCandle = allCandles.OrderByDescending(c => c.GetLength()).FirstOrDefault();

var bigVolCandle = allCandles.OrderByDescending(c => c.TotalVolume).FirstOrDefault();

if (bigPriceCandle != null)

bigPriceCandles.Add(bigPriceCandle);

if (bigVolCandle != null)

bigVolCandles.Add(bigVolCandle);

}

// dibujar series en el gráfico

priceChart.Append("precios", bigPriceCandles.Select(c => c.OpenTime), bigPriceCandles.Select(c => c.GetMiddlePrice(null)), bigPriceCandles.Select(c => c.GetLength()));

volChart.Append("precios", bigVolCandles.Select(c => c.OpenTime), bigPriceCandles.Select(c => c.GetMiddlePrice(null)), bigVolCandles.Select(c => c.TotalVolume));

return Task.CompletedTask;

}

}

}

Código del script en Python

import clr

# Añadir referencias .NET

clr.AddReference("StockSharp.Messages")

clr.AddReference("StockSharp.Algo.Analytics")

clr.AddReference("Ecng.Drawing")

from Ecng.Drawing import DrawStyles

from System.Threading.Tasks import Task

from StockSharp.Algo.Analytics import IAnalyticsScript

from storage_extensions import *

from candle_extensions import *

from chart_extensions import *

from indicator_extensions import *

# Script analítico que muestra la mayor vela (por volumen y longitud) para los instrumentos especificados.

class biggest_candle_script(IAnalyticsScript):

def Run(self, logs, panel, securities, from_date, to_date, storage, drive, format, data_type, cancellation_token):

if not securities:

logs.LogWarning("No hay instrumentos.")

return Task.CompletedTask

price_chart = create_3d_chart(panel, datetime, float, float)

vol_chart = create_3d_chart(panel, datetime, float, float)

big_price_candles = []

big_vol_candles = []

if data_type is None:

logs.LogWarning(f"Tipo de datos no admitido {data_type}.")

return Task.CompletedTask

message_type = data_type.MessageType

for security in securities:

# detener el cálculo si el usuario cancela la ejecución del script

if cancellation_token.IsCancellationRequested:

break

# obtener almacenamiento de velas

candle_storage = get_candle_storage(storage, security, data_type, drive, format)

all_candles = load_range(candle_storage, message_type, from_date, to_date)

if len(all_candles) > 0:

# la primera ordenada por volumen descendente será nuestra vela más grande

big_price_candle = max(all_candles, key=lambda c: get_length(c))

big_vol_candle = max(all_candles, key=lambda c: c.TotalVolume)

if big_price_candle is not None:

big_price_candles.append(big_price_candle)

if big_vol_candle is not None:

big_vol_candles.append(big_vol_candle)

# dibujar series en el gráfico

price_chart.Append(

"precios",

[c.OpenTime for c in big_price_candles],

[get_middle_price(c) for c in big_price_candles],

[get_length(c) for c in big_price_candles]

)

vol_chart.Append(

"precios",

[c.OpenTime for c in big_vol_candles],

[get_middle_price(c) for c in big_price_candles],

[c.TotalVolume for c in big_vol_candles]

)

return Task.CompletedTask