Intraday Volume

The "Intraday Volume" script is a tool for analyzing the distribution of trading volume of securities by hours within a single trading session. Designed for use within the StockSharp platform, it targets traders and quantitative analysts aiming for an in-depth study of market behavior and trading strategy optimization.

Functional Description

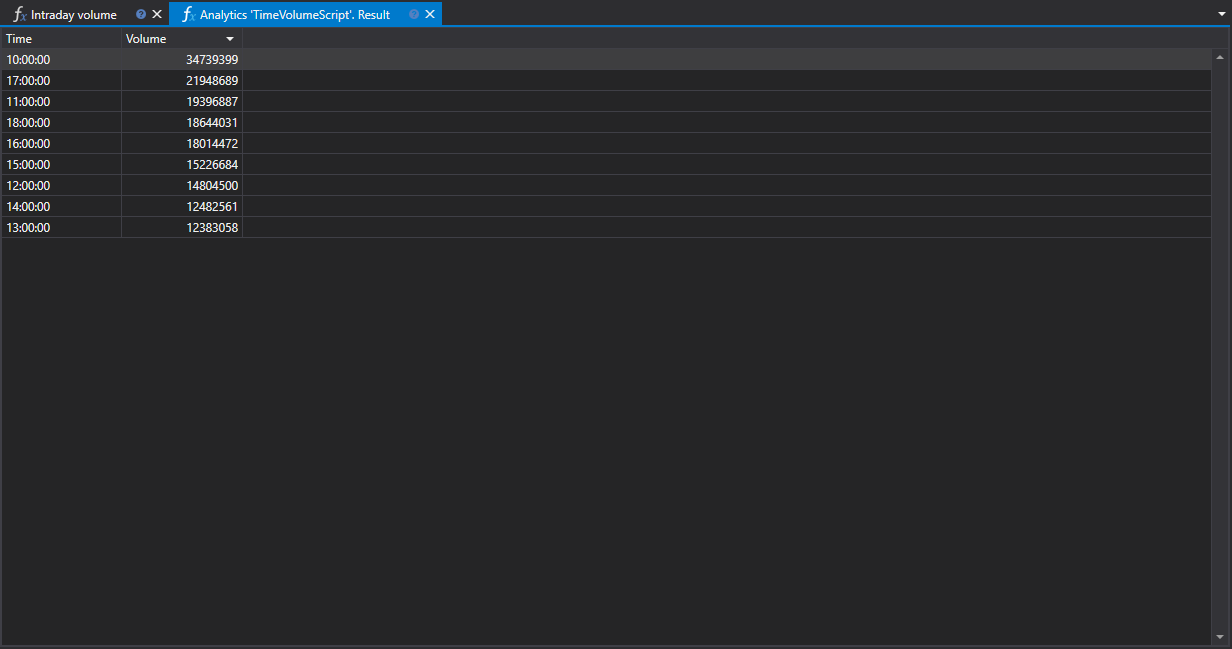

The script collects data on trading operations for a selected time period and presents it in a graph format, allowing users to visualize changes in trading volume by hour. This provides the ability to assess which hours of the day witness increased or decreased trading activity.

Practical Significance

- For Trading: Understanding peak and off-peak hours helps identify the most active market periods, influencing decisions on when to enter or exit positions.

- For Quantitative Analysis: Quant analysts can use intraday volume data to create mathematical models and algorithms predicting market behavior based on volume indicators.

Hourly Distribution

The distribution of trading volume by hour sheds light on market dynamics, highlighting the time intervals with the main trading activity. This may indicate changes in trends, support and resistance levels, as well as potential moments of increased liquidity or its shortage.

Data Application

The "Intraday Volume" script can be integrated into a broader market analysis system, providing data that can be used for:

- Strategy Adaptation: Adjusting trading algorithm parameters according to market activity levels.

- Risk Assessment: Calculating the probability of significant price movements depending on the time of day.

Using the "Intraday Volume" script within the StockSharp trading platform allows traders and analysts to base their decisions on specific data regarding market activity and adapt their strategies to match current trading conditions optimally.

Script Code on C#

namespace StockSharp.Algo.Analytics

{

/// <summary>

/// The analytic script, calculating distribution of the biggest volume by hours.

/// </summary>

public class TimeVolumeScript : IAnalyticsScript

{

Task IAnalyticsScript.Run(ILogReceiver logs, IAnalyticsPanel panel, SecurityId[] securities, DateTime from, DateTime to, IStorageRegistry storage, IMarketDataDrive drive, StorageFormats format, DataType dataType, CancellationToken cancellationToken)

{

if (securities.Length == 0)

{

logs.LogWarning("No instruments.");

return Task.CompletedTask;

}

// script can process only 1 instrument

var security = securities.First();

// get candle storage

var candleStorage = storage.GetCandleMessageStorage(security, dataType, drive, format);

// get available dates for the specified period

var dates = candleStorage.GetDates(from, to).ToArray();

if (dates.Length == 0)

{

logs.LogWarning("no data");

return Task.CompletedTask;

}

// grouping candles by opening time (time part only) with 1 hour truncating

var rows = candleStorage.Load(from, to)

.GroupBy(c => c.OpenTime.TimeOfDay.Truncate(TimeSpan.FromHours(1)))

.ToDictionary(g => g.Key, g => g.Sum(c => c.TotalVolume));

// put our calculations into grid

var grid = panel.CreateGrid("Time", "Volume");

foreach (var row in rows)

grid.SetRow(row.Key, row.Value);

// sorting by volume column (descending)

grid.SetSort("Volume", false);

return Task.CompletedTask;

}

}

}

Script Code on Python

import clr

# Add .NET references

clr.AddReference("StockSharp.Algo.Analytics")

clr.AddReference("StockSharp.Messages")

clr.AddReference("Ecng.Drawing")

from Ecng.Drawing import DrawStyles

from System import TimeSpan

from System.Threading.Tasks import Task

from StockSharp.Algo.Analytics import IAnalyticsScript

from storage_extensions import *

from candle_extensions import *

from chart_extensions import *

from indicator_extensions import *

# The analytic script, calculating distribution of the biggest volume by hours.

class time_volume_script(IAnalyticsScript):

def Run(

self,

logs,

panel,

securities,

from_date,

to_date,

storage,

drive,

format,

data_type,

cancellation_token

):

# Check if there are no instruments

if not securities:

logs.LogWarning("No instruments.")

return Task.CompletedTask

# Script can process only 1 instrument

security = securities[0]

if data_type is None:

logs.LogWarning(f"Unsupported data type {data_type}.")

return Task.CompletedTask

message_type = data_type.MessageType

# Get candle storage

candle_storage = get_candle_storage(storage, security, data_type, drive, format)

# Get available dates for the specified period

dates = get_dates(candle_storage, from_date, to_date)

if len(dates) == 0:

logs.LogWarning("no data")

return Task.CompletedTask

# Grouping candles by opening time (hourly truncation) and summing their volumes

candles = load_range(candle_storage, message_type, from_date, to_date)

rows = {}

for candle in candles:

time_of_day = candle.OpenTime.TimeOfDay

truncated = TimeSpan.FromHours(int(time_of_day.TotalHours))

rows[truncated] = rows.get(truncated, 0) + candle.TotalVolume

# Put our calculations into grid

grid = panel.CreateGrid("Time", "Volume")

for key, value in rows.items():

grid.SetRow(key, value)

# Sorting by Volume column in descending order

grid.SetSort("Volume", False)

return Task.CompletedTask