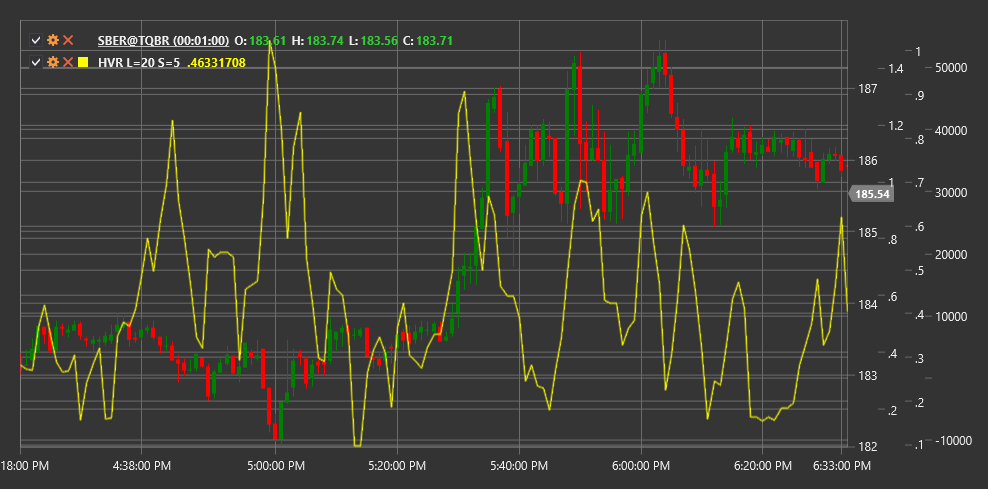

HVR

Historical Volatility Ratio (HVR) is a technical indicator that compares short-term historical volatility with long-term historical volatility to assess changes in market activity.

To use the indicator, you need to use the HistoricalVolatilityRatio class.

Description

The Historical Volatility Ratio (HVR) is a relative volatility indicator that compares short-term volatility with long-term market volatility. The indicator helps determine whether current volatility is increasing or decreasing relative to its historical level.

HVR is calculated as the ratio of short-term historical volatility to long-term historical volatility. Values above 1.0 indicate that current (short-term) volatility is higher than long-term volatility, which may signal increased market activity or a potential trend change.

The indicator is particularly useful for:

- Identifying periods of high and low volatility

- Determining potential trend reversal points

- Adapting trading strategies to current market conditions

- Assessing market risk and setting appropriate position sizes

Parameters

The indicator has the following parameters:

- ShortPeriod - period for calculating short-term volatility (default value: 5)

- LongPeriod - period for calculating long-term volatility (default value: 20)

Calculation

Historical Volatility Ratio calculation involves the following steps:

Calculate short-term historical volatility:

Short-term Volatility = Standard Deviation of Log Returns over ShortPeriod * Sqrt(Trading Days Per Year)Calculate long-term historical volatility:

Long-term Volatility = Standard Deviation of Log Returns over LongPeriod * Sqrt(Trading Days Per Year)Calculate HVR as the ratio of short-term volatility to long-term volatility:

HVR = Short-term Volatility / Long-term Volatility

Where:

- Log Returns - logarithmic returns (ln(Price[i] / Price[i-1]))

- Standard Deviation - standard deviation

- Trading Days Per Year - number of trading days in a year (usually 252 for stock markets)

- ShortPeriod - short period for volatility calculation

- LongPeriod - long period for volatility calculation

Interpretation

The Historical Volatility Ratio can be interpreted as follows:

Level 1.0:

- HVR = 1.0 means short-term volatility is equal to long-term volatility

- HVR > 1.0 indicates short-term volatility is higher than long-term volatility

- HVR < 1.0 indicates short-term volatility is lower than long-term volatility

Extreme Values:

- Very high HVR values (e.g., > 2.0) may indicate a sharp volatility increase, often occurring during market panics or strong movements

- Very low HVR values (e.g., < 0.5) may indicate a volatility compression period, often preceding strong movements

HVR Trends:

- Rising HVR indicates an increase in current volatility

- Falling HVR indicates a decrease in current volatility

Trading Strategies:

- When HVR is high, it may be appropriate to use breakout-based strategies

- When HVR is low, mean reversion or range trading strategies may be more suitable

Risk Management:

- High HVR values may signal the need to reduce position sizes due to increased volatility

- Low HVR values may allow increased position sizes due to reduced volatility

Potential Reversals:

- Extreme HVR values often precede significant price movements

- A sharp HVR increase after a low volatility period may signal the start of a new trend